Army Healthcare: TRICARE Explained for New Soldiers

Most people shopping for a new job look at the health insurance section of the offer letter first. When you join the Army, that section is short: you’re covered. But what that actually means in practice, for you and your family, takes more explaining than a one-pager can hold.

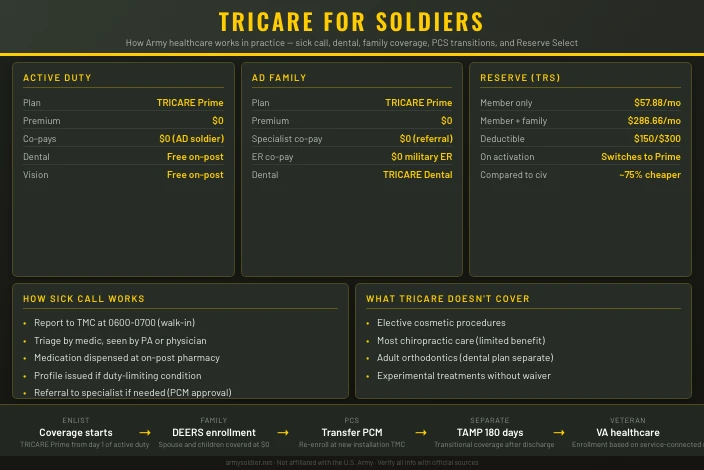

TRICARE is the health insurance program for the U.S. military. Active duty soldiers use a version called TRICARE Prime, which works like a managed care plan: you have a primary care manager who coordinates your care, and you pay nothing for covered services at in-network providers. No premiums, no deductibles, no copays for standard in-network care.

For a family of four, that math hits differently than the typical civilian job offer.

What TRICARE Actually Covers

Active duty service members get full medical coverage at no cost. That part is simple. The coverage list for TRICARE Prime is broad:

- Doctor visits and specialist referrals

- Emergency and urgent care

- Mental health services

- Prescriptions (free at military pharmacies and TRICARE Home Delivery)

- Hospitalization and surgery

- Maternity and newborn care

- Preventive care and immunizations

Family members enroll under the sponsor (the service member) at no cost. There are no enrollment fees and no copays when your spouse or kids use in-network TRICARE Prime providers. The annual catastrophic cap for active duty families is $1,000, meaning that’s the most your family will pay out-of-pocket in a calendar year under normal circumstances.

The one trap to know: if a family member goes outside the network without a referral, that’s the Point-of-Service option. It triggers a 20% cost-share after a $300 individual or $600 family deductible. Stay in-network and follow the referral process and that never applies.

How Sick Call Actually Works

Sick call exists for exactly what the name implies: you woke up sick and need to be seen today. Most installations run sick call early in the morning, typically before regular duty hours. You show up, get triaged, and see a provider. No appointment needed, no copay.

What sick call is not: a place for follow-up visits, prescription renewals, or chronic condition management. Those get handled through your Primary Care Manager during scheduled appointments. Treating sick call like a general clinic frustrates everyone and slows the process for soldiers who genuinely need it.

For family members, the MTF (Military Treatment Facility) is the first stop when they’re enrolled in TRICARE Prime and live near an installation. Active duty family members get priority for care at MTFs after active duty service members themselves. Availability depends on the installation. At larger posts with major medical centers, like Fort Sam Houston or Fort Campbell, the MTF can handle most primary and specialty care on-post.

At smaller installations or in areas with limited MTF capacity, your family sees civilian providers in the TRICARE network. The coverage works the same way. The experience looks more like a regular doctor’s office visit, because it is one.

Dental and Vision: The Reality

This is where new soldiers get surprised.

Dental for active duty service members is handled by the military itself, not TRICARE. Your unit will direct you to the installation dental clinic for routine care. It’s free, but appointments can be slow and access depends heavily on the installation.

For your family, dental is a separate program called the TRICARE Dental Program (TDP), and it is not automatic. You have to enroll them, and there is a monthly premium:

| Coverage | E-4 and Below | E-5 and Above |

|---|---|---|

| Member only | $8.65/mo | $11.53/mo |

| Family | $22.48/mo | $29.98/mo |

The annual benefit maximum is $1,500 per person for non-orthodontic services. Orthodontic coverage carries a lifetime maximum of $1,750 per person. That’s workable for routine cleanings and fillings. It’s not a plan that covers a full set of braces without any out-of-pocket costs.

Vision for active duty is covered as a readiness function. Exams are provided as needed to maintain fitness for duty. If you need glasses, the military will issue them, though the frames are notoriously basic.

For family members, TRICARE covers one routine eye exam per year under all plans. It does not cover glasses or contact lenses as a standard benefit. Families who need more than a basic annual exam typically buy a separate vision plan or pay out of pocket.

What Happens When You PCS

PCS season creates more TRICARE questions than almost anything else. The short answer: your coverage doesn’t stop.

TRICARE travels with you. Your family’s medical, dental, and pharmacy coverage remain active during a move. But there are a few things to do before and after to avoid friction.

Before your PCS:

- Request copies of medical and dental records at least one month before your report date. Hand-carry them to your new installation.

- Schedule any pending appointments, fill prescriptions to last through the move period, and handle any referrals in progress.

- Do not disenroll from your current plan before the move.

After you arrive:

- Update your address in DEERS (Defense Enrollment Eligibility Reporting System). This is what tells TRICARE where you are.

- You have 90 days from your address change to update or change your TRICARE plan and region.

PCSing is a Qualifying Life Event, which means you can enroll or make changes to your plan outside of Open Season. If you move from a TRICARE Prime service area to a location where Prime isn’t available, your family will transition to TRICARE Select, which functions more like a PPO. You can choose any TRICARE-authorized provider without a referral, but cost-sharing applies.

Coverage During Deployment

When a soldier deploys, family members’ coverage stays fully intact. Active duty family members remain TRICARE-eligible regardless of where the sponsor is stationed or deployed. The key step is making sure DEERS is current before the soldier leaves.

If the family is moving to a different location while the soldier is deployed, coverage transitions follow the same PCS rules. If they stay put, nothing changes for them at all.

For Reserve soldiers called to active duty for more than 30 days, full TRICARE eligibility kicks in for both the soldier and their family. That coverage ends when the orders end, though there’s a short continuation window afterward. Reserve families who were enrolled in the TRICARE Dental Program before activation can continue that coverage during the deployment period.

TRICARE Reserve Select for Part-Timers

Guard and Reserve members who aren’t on active duty orders can purchase TRICARE Reserve Select (TRS), a premium-based plan that provides coverage similar to TRICARE Select.

Monthly premiums for 2026:

| Coverage | Monthly Premium |

|---|---|

| Member only | $57.88 |

| Member + family | $286.66 |

At under $300 a month for a family, TRS is significantly cheaper than most civilian employer plans. It’s not free, but the cost is a substantial benefit compared to what comparable civilian coverage runs.

TRS does require a cost-share for care, unlike the zero-copay structure active duty members enjoy. For Reserve soldiers who also have civilian employer insurance available, comparing both plans before deciding is worth doing. Sometimes the employer plan’s network is better. Sometimes TRS wins on price by a wide margin.

How It Stacks Up Against Civilian Coverage

The civilian comparison matters because many recruits are choosing between a job offer and Army service. The numbers are stark.

The KFF 2025 Employer Health Benefits Survey puts the average annual family premium for employer-sponsored coverage at $26,993, with workers paying an average of $6,850 of that themselves. Most plans carry deductibles of $1,000 or more before insurance covers anything.

TRICARE Prime for an active duty family: $0 in premiums, $0 in deductibles, $1,000 annual catastrophic cap.

That gap is not small. For a family of four, premium savings alone can exceed $6,000 per year compared to what a civilian counterpart pays. That number doesn’t show up on your LES, but it’s real compensation.

A few limitations are worth naming honestly:

- PCM assignment. You don’t choose your primary care manager the way you’d pick a doctor in a civilian HMO. You get assigned based on availability at your MTF.

- Specialty care wait times. Referrals and appointments at busy MTFs can stretch out. Soldiers at posts with smaller medical facilities sometimes wait longer for specialist access.

- Geographic constraints. TRICARE Prime isn’t available in every location. Soldiers stationed in remote areas may have fewer provider choices and end up in TRICARE Prime Remote.

None of these are dealbreakers. They’re the honest tradeoffs compared to a civilian plan where you can typically pick any in-network doctor on day one.

What Changes When You Separate

TRICARE eligibility ends when you leave active duty, with a brief continuation window. Soldiers who served at least 20 years retire and retain TRICARE benefits for life. Those separating earlier have transition options, including TRICARE Transitional Assistance Management Program (TAMP), which extends coverage for 180 days after separation.

After TAMP ends, separating soldiers and their families can purchase TRICARE Young Adult for dependents up to age 26, or transition to civilian coverage through the marketplace.

Veterans with service-connected disabilities may also qualify for VA healthcare, which runs separately from TRICARE. Priority and eligibility for VA care depend on disability rating and service history.

The Army benefits guide covers the full picture of compensation, allowances, and what you’re entitled to beyond healthcare.

You may also find the complete guide to Army pay and benefits, how BAH housing allowance works, and what the Post-9/11 GI Bill covers helpful for understanding the full financial picture of Army service.

This site is not affiliated with the U.S. Army or any government agency. Verify all information with official Army sources before making enlistment or career decisions.