Army Retirement: BRS Pension Calculator and Timeline

At the eight-year mark, the math starts to feel real. You’re halfway to a pension, you’ve got seniority and skills, and the civilian world is calling. The decision to stay or go is one of the biggest financial choices in a military career, and most people make it without ever running the actual numbers.

This post walks through exactly what BRS looks like in dollars: how the TSP match compounds over time, what continuation pay is worth, and what a 20-year E-7 pension actually pays each month. If you’ve seen the official briefings but still aren’t sure whether staying makes financial sense, this is for you.

What the Blended Retirement System Actually Is

BRS replaced the legacy High-3 system for anyone who entered service after January 1, 2018. Soldiers already serving had a one-time window to opt in. If you joined after that date, you’re in BRS automatically.

The system has three moving parts:

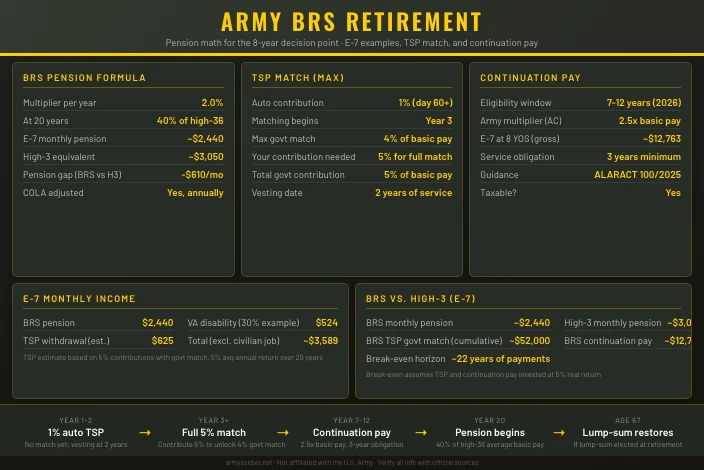

- Pension: Monthly annuity starting at 20 years, calculated at 2% per year of service

- TSP match: Government contributions to your Thrift Savings Plan account, up to 5% of basic pay

- Continuation pay: A mid-career lump-sum bonus paid between 7 and 12 years of service

The key difference from legacy High-3 is the pension multiplier. Legacy used 2.5% per year; BRS uses 2.0% per year. That gap is real and it matters. A 20-year retiree gets 40% of their high-36 average pay under BRS versus 50% under High-3. The trade-off is the TSP match, which High-3 soldiers never received.

The “high-36” basis means your pension is calculated on the average of your highest 36 consecutive months of basic pay, not your pay on retirement day. For most people retiring at exactly 20 years, those 36 months are close to the same number.

The TSP Match: Why the First Three Years Matter Most

The automatic 1% contribution starts after 60 days of service. The matching contributions (up to 4% more) begin at the start of your third year. Both vest at two years, meaning the government’s contributions become yours to keep once you pass that mark.

To get the full government contribution, you need to contribute 5% of your basic pay to your TSP. Here’s what that looks like at different points in an enlisted career:

| Rank | YOS | Basic Pay | Your 5% | Govt Match | Total Monthly |

|---|---|---|---|---|---|

| E-4 | 3 | $3,483 | $174 | $174 | $348 |

| E-5 | 6 | $4,109 | $205 | $205 | $411 |

| E-6 | 10 | $4,759 | $238 | $238 | $476 |

| E-7 | 14 | $5,537 | $277 | $277 | $553 |

That matching column is free money. A soldier who never contributes to TSP still gets the 1% auto contribution. But they leave the other 4% on the table every single month.

The compounding matters more than the monthly amount. A 22-year-old who starts contributing 5% and maintains it through 20 years will have substantially more in their TSP at retirement than someone who waits until year five to start. The government match doesn’t retroactively fill the gap.

One practical note: TSP contributions follow the same IRS limits as civilian 401(k) plans. The 2026 elective deferral limit is $23,500 for those under 50. Most junior enlisted members won’t come close to hitting that ceiling, but it becomes relevant for senior NCOs with high deployment pay.

The Eight-Year Decision: What Staying Actually Costs You

Here’s the honest version of the 8-year math.

You’ve served eight years. You have marketable skills: a clearance, leadership experience, technical training. The civilian market will pay for those. But you’re also 12 years from a pension that pays for life.

The question isn’t whether a 20-year pension is valuable. It is. The question is what you give up to get there.

What you’re trading:

- 12 more years of active duty service

- Geographic instability, deployments, and time away from family

- Civilian career earnings during prime earning years (roughly ages 26-38)

What you get:

- Monthly pension for life starting the day you retire

- TRICARE retirement coverage for you and dependents

- Post-9/11 GI Bill (if not already used)

- 30% VA disability compensation stacked on top, if applicable

The pension is the centerpiece. Let’s put real numbers on it.

An E-7 retiring at 20 years with a high-36 average basic pay of approximately $6,100 per month receives:

2% x 20 years x $6,100 = $2,440/month

That’s $29,280 per year, for life, with annual cost-of-living adjustments. It’s not enough to live on alone in most markets, but combined with a civilian job, VA disability, and TSP withdrawals, it creates a floor most civilian workers don’t have.

Compare that to the legacy High-3 formula that someone who had the choice might have passed up:

2.5% x 20 years x $6,100 = $3,050/month

The BRS pension is $610 per month lower at the 20-year mark for the same rank and service length. Over a 30-year retirement, that adds up to roughly $220,000 in forgone pension income before COLA adjustments. Whether the TSP match offsets that depends entirely on how aggressively the soldier invested.

Continuation Pay: Take It or Negotiate It

Continuation pay is a lump-sum bonus available to BRS members between 7 and 12 years of service (changed from 8-12 starting in 2026 per ALARACT 100/2025). In exchange, you commit to at least three additional years of active duty service.

For Army active component soldiers, the standard multiplier is 2.5 times monthly basic pay. An E-7 at 8 years of service earns $5,105 per month, which means:

2.5 x $5,105 = $12,763 gross

That’s a one-time taxable payment. After federal taxes at a typical withholding rate, expect to take home roughly $9,500-10,000 depending on your filing status.

A few things worth knowing before accepting:

- You can request continuation pay early, at 7 years, but you can’t game the multiplier by waiting for a promotion. The multiplier is fixed by service directive, not rank.

- The 3-year obligation is the floor. Some career fields may have additional retention incentives tied to continuation pay acceptance.

- Put it in TSP if you can. Continuation pay is a windfall. Dumping it into a taxable account and spending it defeats the purpose. Contributing up to the annual IRS limit in the year you receive it accelerates your retirement savings significantly.

- Don’t count on higher multipliers. The Army had flexibility to offer up to 13x in some years. ALARACT 100/2025 standardized the active component rate at 2.5x for 2026.

If you’re at the 7-8 year mark and actively weighing separation, accepting continuation pay and then separating at the 10-year mark is not an option. The service obligation is real and enforced.

The Lump-Sum Option at Retirement

BRS introduced a lump-sum election that legacy High-3 never had. At retirement, you can elect to receive 25% or 50% of your projected lifetime pension value upfront as a lump sum. In exchange, your monthly annuity is reduced until age 67, when it restores to the full amount.

The math generally does not favor taking the lump sum unless you have a specific investment purpose for it. The discount rate the government uses to calculate the lump sum is typically less favorable than what a disciplined investor could earn over the same period. Most financial planners advise against it for healthy retirees with a normal life expectancy.

If you’re considering it, Army retirement pay details on the benefits guide walk through the actuarial basis in more detail.

BRS vs. High-3: For Those Who Had the Choice

Soldiers already serving when BRS launched in 2018 had an opt-in window. Those who stayed on legacy High-3 kept the 2.5% multiplier but received no TSP matching. The math on which choice was better depends on three variables: how long you served, how much you contributed to TSP, and what your investment returns were.

Here’s a clean comparison for an E-7 retiring at 20 years:

| Legacy High-3 | BRS | |

|---|---|---|

| Monthly pension | ~$3,050 | ~$2,440 |

| TSP government match | $0 | ~$52,000 cumulative (est.) |

| Continuation pay | $0 | ~$12,763 |

| Break-even horizon | – | ~22 years of pension payments |

The break-even assumes the TSP match and continuation pay are invested and grow at a modest 5% real return. If the TSP was left in the G Fund earning 3-4%, the break-even extends significantly. If it was invested in a broad index fund over 20 years, the math favors BRS for most soldiers.

For those who did opt in to BRS in 2017-2018 and are now approaching retirement, the key question is whether you consistently contributed 5% throughout your career. If you didn’t, especially in the first three to five years, the TSP match advantage shrinks considerably.

What a 20-Year Retirement Actually Looks Like Month to Month

Pension math looks abstract until you see it stacked with other income sources. Here’s a realistic monthly picture for an E-7 retiring at 20 years:

| Income Source | Monthly Amount |

|---|---|

| BRS pension | $2,440 |

| VA disability (30%, example) | $524 |

| TSP withdrawal (5% of $150K balance) | $625 |

| Part-time or civilian job | Varies |

| Total (before civilian work) | ~$3,589 |

That TSP balance estimate assumes consistent 5% contributions with government match starting at year three and a conservative 5% average annual return. A soldier who invested more aggressively or contributed extra above the match would have a larger balance.

The complete guide to Army pay and benefits has a broader breakdown of how these income streams interact with taxes and VA compensation.

Retirement healthcare changes at 20 years too. Active-duty TRICARE Prime transitions to TRICARE Retired Reserve or TRICARE Select depending on age and status. Before age 65, retirees pay premiums. BRS retirees (Group B) pay roughly $595 per year for individual TRICARE Select enrollment in 2026. That’s a meaningful change from zero-cost active-duty coverage.

The Real Answer to “Is Army Retirement Worth It”

For most people, yes. But not for the reasons the recruiting poster says.

The pension itself, at $2,400-$2,500 per month for an E-7, is modest. It won’t replace a full income. What makes it powerful is that it’s guaranteed, inflation-adjusted income that starts immediately at age 38-42 for most enlisted retirees. No vesting period. No market risk. No employer bankruptcy. It shows up every month.

Combined with VA disability, TSP savings, the GI Bill, and a second career, the 20-year package creates financial stability that most civilian workers spend a lifetime trying to build. The trade-off is 12 years of service beyond the 8-year mark: missed family events, moves, deployments, and constraints that civilian peers don’t face.

The math alone won’t make the decision for you. But running the actual numbers, not estimates, is the right place to start.

You may also find the Army officer vs. enlisted pay comparison useful if you’re considering an OCS application alongside the retirement decision, and the Army benefits guide covers retirement eligibility rules and TRICARE transition details in full.

This site is not affiliated with the U.S. Army or any government agency. Verify all information with official Army sources before making enlistment or career decisions.