Complete Guide to Army Pay and Benefits (2026)

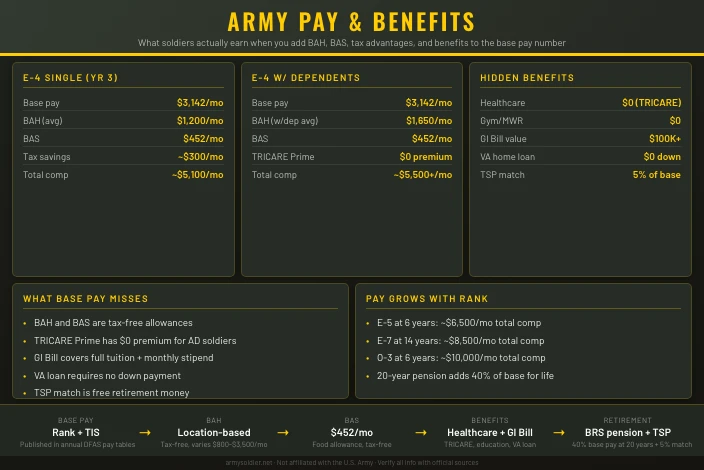

Most online searches for “Army pay” return a basic pay table and stop there. That number – say, $3,142 per month for a new Specialist (E-4) – is real, but it’s also incomplete. Add housing allowance, food allowance, free healthcare, and the tax treatment on those allowances, and the actual compensation picture looks very different. For a Specialist with dependents stationed at a mid-cost installation, total compensation clears $5,500 a month before a single benefit like healthcare or free on-post gym access is counted.

This post breaks down how Army compensation actually works – layer by layer, life situation by life situation – so you can evaluate it against a civilian paycheck the right way.

How Army Pay Is Actually Built

Army pay has three cash components that apply to almost every soldier. Understanding each one matters because they’re taxed differently and valued differently depending on your situation.

Basic pay is the taxable foundation. It’s set by pay grade (rank) and years of service. Everyone at the same grade and service time earns the same basic pay, whether they’re a cook or a combat engineer.

Basic Allowance for Subsistence (BAS) is a flat monthly food allowance. Enlisted soldiers receive $476.95 per month in 2026. It doesn’t vary by rank, location, or family size – every enlisted soldier gets the same amount. Officers receive $328.48.

Basic Allowance for Housing (BAH) is where the real money often hides. It’s tax-free, it scales with pay grade and dependency status, and it varies by duty station based on local rental market data. At a mid-cost installation like Fort Sam Houston in San Antonio, an E-4 without dependents receives $1,359 per month. An E-4 with dependents receives $1,728 per month.

That $369 monthly gap between dependent and non-dependent BAH adds up to $4,428 per year – all tax-free – purely because of family status.

What “Tax-Free” Actually Means

BAH and BAS are not taxed as income. For a soldier in the 22% federal tax bracket, every dollar of tax-free allowance is worth about $1.28 compared to a taxable civilian dollar. A civilian earning $1,728 per month in gross housing pay would net roughly $1,348 after federal income tax. The soldier keeps all $1,728.

This tax advantage compounds at higher ranks. An E-7 with dependents stationed in a high-cost area can receive well over $2,500 in tax-free BAH monthly. Matching that in civilian gross income requires earning closer to $3,200 before taxes in a 22% bracket.

On-Post Housing: A Different Calculation

Soldiers who live on post don’t receive BAH as cash – it goes directly to the housing provider. The practical effect is zero housing cost with no out-of-pocket payment. For a young soldier without strong savings or credit history, access to quality housing without a security deposit, credit check, or lease risk has real economic value that doesn’t show up in any pay table.

E-4 Total Compensation: Single vs. With Dependents

Here’s what a Specialist with two years of service actually takes home, using Fort Sam Houston as the duty station example.

| Component | Single E-4 | E-4 with Dependents |

|---|---|---|

| Basic pay (2 years) | $3,303/mo | $3,303/mo |

| BAS | $477/mo | $477/mo |

| BAH (Fort Sam Houston) | $1,359/mo | $1,728/mo |

| Cash total | $5,139/mo | $5,508/mo |

| Tax-free portion | $1,836/mo | $2,205/mo |

| Taxable portion | $3,303/mo | $3,303/mo |

The “base salary” of $3,303 sounds modest. The full cash package – $5,139 for a single soldier, $5,508 for one with dependents – tells a more complete story. Both figures exclude the value of free healthcare, dental, vision, and retirement contributions.

A civilian job paying $55,000 per year ($4,583/mo gross) might look like more money. But that civilian also pays federal and state income taxes on the full amount, covers their own health insurance premiums, and funds their own housing. The after-tax, after-benefits comparison is much closer than the headline numbers suggest.

How Benefits Compound Over a Career

Basic pay increases with every promotion and every two years of service. The non-cash benefits – healthcare, education, retirement – don’t change in cost to you, but their value grows as you compare them against what you’d pay in the civilian world.

Healthcare: Zero Out of Pocket

Active duty soldiers and their families receive TRICARE Prime at no cost. No enrollment fee. No deductible. No copay for in-network care. A family of four on a comparable civilian employer plan typically pays $400 to $800 per month in premiums, plus deductibles and copays on top. Over a four-year enlistment, that’s $19,000 to $38,000 in avoided healthcare costs – money that never leaves your paycheck because you never had to spend it.

The full breakdown of TRICARE coverage explains what active duty, Reserve, and post-service options look like.

Education: Two Separate Programs

The Army funds college in two different ways, and most soldiers use both.

Tuition Assistance (TA) covers $4,500 per year while you’re on active duty. You take classes on your own time, the Army pays your tuition directly, and your paycheck doesn’t change. Soldiers working toward a degree during their enlistment regularly finish with no student loan debt.

The Post-9/11 GI Bill activates after separation for soldiers who served at least 90 days on active duty after September 10, 2001. At the 100% benefit level (36 months active duty or more), it covers full in-state tuition and fees at any public university with no dollar cap. Private school tuition is covered up to $29,920.95 for the 2025-2026 academic year. On top of that, you receive a monthly housing allowance based on the E-5-with-dependents BAH rate at your school’s ZIP code – which at many major universities runs $1,500 to $2,200 per month. You also get $1,000 per year for books.

A four-year degree at a state school paid entirely by the GI Bill, with a $1,800/month housing allowance while you’re attending, represents a benefit worth $100,000 or more depending on your location and school. What the Post-9/11 GI Bill covers walks through the eligibility rules and how to calculate your specific benefit.

Pay Raises: Promotion and Longevity

Basic pay doesn’t stay flat. Two forces push it up over a career.

Promotion raises are significant. An E-4 earning $3,303 per month at two years of service who promotes to E-5 (Sergeant) jumps to at least $3,343 at the time of promotion – and those rates increase further with additional service. An E-5 at eight years earns $4,299 per month in basic pay. Pair that with higher BAH rates at E-5 and the compensation gap versus an entry-level civilian grows wider every year.

Annual across-the-board raises are set by Congress. In 2026, the raise was 3.8% across all grades. These annual increases compound – a soldier who serves 10 years receives nine separate pay raises on top of their promotion raises.

| Grade | Years of Service | Basic Pay |

|---|---|---|

| E-4 | 2 years | $3,303/mo |

| E-5 | 4 years | $3,947/mo |

| E-6 | 8 years | $4,613/mo |

| E-7 | 12 years | $5,537/mo |

The Retirement Math

Twenty years of service earns a pension. Under the Blended Retirement System (BRS) – which applies to anyone who entered service after January 1, 2018 – a soldier who serves exactly 20 years receives 40% of their average highest 36 months of basic pay, paid monthly for life, starting the day they leave the Army.

For an E-7 retiring at 20 years, that average high-36 might be around $5,000 to $5,300 per month. At 40%, the pension runs $2,000 to $2,120 per month for life, with no requirement to keep working. That pension kicks in at age 38 or 40 for most enlisted soldiers who served from their late teens or early twenties.

BRS also includes Thrift Savings Plan (TSP) matching. The Army automatically contributes 1% of your basic pay into a TSP account starting after 60 days of service. Beginning in your third year, if you contribute at least 5% of your own pay, the Army adds another 4% – a 5% total government contribution to your retirement account. Over a 20-year career, consistent TSP contributions plus government matching can build a substantial investment account alongside the pension.

The Army retirement and BRS pension calculator runs the full math, including lump-sum options and the impact of TSP contribution rates at different pay grades.

30-Day Leave and What It Actually Gets You

Soldiers earn 30 days of paid vacation per year – 2.5 days per month. Most civilian jobs offer 10 to 15 days in the first few years, with 20 days considered generous. The Army’s leave benefit is better than most private sector employers from day one, and it’s in addition to 11 federal holidays.

Leave can carry over up to 60 days, making it possible to bank time for longer trips or terminal leave before separation. A soldier leaving active duty with 60 days banked gets two full months of continued pay after their last duty day.

Special Pays on Top of Base

Certain assignments trigger additional monthly pay on top of the standard package. These don’t apply to everyone, but they’re common enough to factor into career planning.

- Combat Zone Tax Exclusion: All military pay earned during a deployment to a designated combat zone is exempt from federal income tax. For an E-5 earning $3,776 in basic pay, that’s over $830 per month in federal income tax that simply doesn’t exist during deployment.

- Hazardous Duty Incentive Pay (HDIP): Parachutists, combat divers, and flight crew members receive monthly HDIP ranging from $150 to $250.

- Special Duty Assignment Pay (SDAP): Drill Sergeants, Recruiters, and similar high-demand roles receive up to $375 per month in extra pay.

- Enlistment and reenlistment bonuses: Some MOS receive lump-sum bonuses at enlistment or when reenlisting. Amounts vary by MOS, current Army needs, and contract length.

Reserve and National Guard Pay: A Different Equation

Reserve and National Guard soldiers don’t receive a full-time salary, BAH, or BAS. Pay is based on the number of drill periods completed. A standard month includes one weekend (four drill periods) plus annual training, totaling about 62 paid days per year.

The financial trade-off is straightforward: part-time service at a part-time pay rate, but with access to some full-time benefits. Reserve soldiers who have served the required years and are activated to full-time status can qualify for GI Bill benefits under the same eligibility rules. Health insurance through TRICARE Reserve Select is available at a monthly premium – not free, but significantly cheaper than individual civilian plans.

Reserve soldiers mobilized to active duty receive the same full pay, BAH, and BAS as their active component counterparts for the duration of the deployment.

The active duty vs. Army Reserve comparison lays out the full financial and lifestyle differences between the two options.

What the Numbers Add Up To

Run the numbers on a single E-4 at two years of service, at Fort Sam Houston, with free on-post healthcare and no student loan debt from TA-funded coursework:

- Cash compensation: $5,139/month ($61,668/year)

- Avoided healthcare cost: ~$600/month equivalent ($7,200/year)

- TSP automatic contribution (1%): ~$33/month

- Combined value: roughly $69,000 per year before any GI Bill, leave value, or special pays

A 22-year-old civilian with a bachelor’s degree and 0-2 years of experience in most markets earns less than that in total compensation – and often carries $30,000 or more in student loan debt on top. The comparison isn’t as one-sided as the base pay number makes it look.

The Army benefits overview has reference tables for pay charts, BAH rate lookups, and eligibility rules across every benefit category. For a side-by-side look at how total compensation changes when you go the officer route, Army officer vs. enlisted pay runs the same analysis at every career milestone. You may also find Army BAH rates and how housing allowance works helpful for understanding how your specific duty station affects the numbers.

This site is not affiliated with the U.S. Army or any government agency. Verify all information with official Army sources before making enlistment or career decisions.