Post-9/11 GI Bill: What It Covers and How to Use It

Most soldiers know the GI Bill pays for college. Far fewer know that the school you pick, the city it’s in, and how many months you served can swing your total benefit by tens of thousands of dollars. The difference between a smart GI Bill strategy and a poor one isn’t eligibility. It’s math.

What the GI Bill Actually Pays

The Post-9/11 GI Bill (Chapter 33) has three separate payment streams. Each one works differently, and each has its own ceiling.

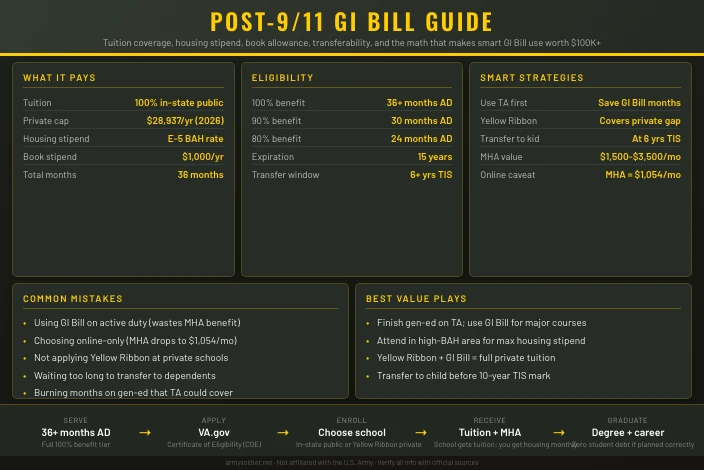

Tuition and fees go directly to the school. For public in-state universities, the VA pays the full bill with no dollar cap. For private schools and out-of-state programs, the VA caps its payment at $29,920.95 per academic year (2025-2026 rate), rising to $30,908.34 starting August 1, 2026. Private school tuition regularly runs $40,000 to $60,000 per year, which means you’d face a gap of $10,000 or more annually without additional coverage.

Monthly Housing Allowance (MHA) is paid directly to you while you’re enrolled. It equals the BAH rate for an E-5 with dependents at the zip code of your school. A soldier attending UT Austin collects a different MHA than one attending Penn State, because local housing costs vary. The national average runs around $2,200 to $2,500 per month for in-person students. If you take all your classes online, the rate drops to a flat $1,169 per month nationwide, regardless of location.

Books and supplies stipend pays up to $1,000 per academic year, or up to $41.67 per credit hour for up to 24 credits. It’s not large, but it’s automatic once you’re enrolled.

| Payment Type | Public School | Private School |

|---|---|---|

| Tuition | 100% of in-state tuition | Up to $29,920.95/year |

| MHA (in-person) | E-5 w/dep BAH at school ZIP | Same |

| MHA (online only) | $1,169/month flat | $1,169/month flat |

| Books/supplies | Up to $1,000/year | Up to $1,000/year |

The MHA stops during summer breaks unless you’re enrolled in classes. That gap catches a lot of people off guard.

The Real Math by School Type

The school you choose changes the GI Bill’s effective value by a wide margin. A few concrete scenarios show the spread.

State university (in-state) is the full-coverage scenario. Tuition, mandatory fees, MHA, and the book stipend are all covered. At a school in a mid-cost city, you might net $2,200 per month in housing while paying nothing out of pocket for classes. Over 36 months (the maximum benefit), that’s roughly $79,000 in housing payments alone, plus fully covered tuition.

Private university without Yellow Ribbon requires careful math before you commit. If a private school charges $55,000 per year in tuition, the VA pays $29,920.95 and you cover the remaining $25,000 yourself. Over four years, that gap reaches $100,000, most of it probably in student loans.

Private university with Yellow Ribbon can close that gap entirely at participating schools. The school waives a portion of the excess tuition, and the VA matches dollar-for-dollar. A school that contributes $12,500 toward the gap gets a $12,500 VA match, eliminating $25,000 of shortfall. Full-coverage Yellow Ribbon schools exist, but they’re selective. Each school sets its own cap on how many students it accepts into the program per year.

Trade school or vocational program is the highest net-value scenario for total monthly cash flow. The VA pays actual net costs up to the private school cap, and most trade programs cost far less than the cap. The MHA still applies.

Community college gives full coverage of in-state tuition with MHA at the local rate. The math is straightforward and favorable.

A state university or trade school delivers the most total dollar value. A private school without Yellow Ribbon can cost six figures out of pocket despite having the GI Bill.

How the Housing Stipend Works

The MHA is calculated at enrollment, not at discharge. The VA looks up the BAH rate for an E-5 with dependents at the primary campus zip code. If your school spans multiple campuses, the location where you take the majority of your credit hours determines the rate.

A few mechanics that matter:

- Enrollment status affects your rate. Full-time enrollment pays the full MHA. Half-time pays half. Less than half-time pays nothing.

- The rate resets each August. Your MHA can go up or down each academic year as national BAH rates change.

- Online-only triggers the flat rate. If even one class is in-person, you keep the local rate. The flat $1,169 only kicks in when every credit that term is delivered online.

- The VA pays in arrears. Your housing payment for October arrives in November. Budget for that lag at the start of each semester.

- Summer breaks are unpaid. No enrollment means no MHA. Summer classes do count against your benefit total, but you receive MHA while enrolled in them.

A soldier attending UT Austin full-time in person would pull close to $2,400 per month in MHA. That same soldier taking all classes online would receive $1,169. The delivery method is a financial decision, not just a scheduling one.

Yellow Ribbon: How the Gap Coverage Actually Works

Yellow Ribbon is not automatic and not guaranteed. The program is voluntary. Schools opt in each year and set their own terms.

Each participating school specifies three things: the maximum dollar amount it will contribute per student per year, the number of students it will cover, and which degree programs qualify. A school might offer unlimited spots at unlimited contribution (some large universities do this), or it might offer five spots at $3,000 per student for graduate programs only.

To qualify for Yellow Ribbon coverage:

- Qualify at 100% benefit level. That means 36 or more months of active duty service after September 10, 2001. Purple Heart recipients and those discharged with service-connected disabilities also qualify at 100% regardless of service length.

- Apply to a participating school. VA’s Yellow Ribbon school finder shows current participants. Schools can join or leave the program each year.

- Be admitted and enrolled. Yellow Ribbon only applies to amounts above the annual private school cap. It does not stack if you’re below 100% benefit level.

The VA opens Yellow Ribbon enrollment for the next academic year between March 15 and May 15. Schools finalize their agreements before August 1. If you’re planning to attend a private school, check current participation status and spot availability before you apply, not after you receive an acceptance letter.

Transferring Benefits to Dependents

The transferability rules are strict, and the most common mistake is waiting too long.

You can transfer your GI Bill to a spouse or children if you have at least six years of service and agree to serve four additional years from the date of transfer approval. The transfer request must be submitted and approved while you’re still on active duty. Submitting after you separate is not possible, regardless of total years served.

The DEERS timing trap: Many service members plan to transfer benefits but never formally designate months in the milConnect system while they’re active. When they try to add dependents after separation, the system blocks them. The fix is simple: while still active, log into milConnect and assign at least one month of benefits to each dependent you might want to cover. You can always adjust the allocation later, but you cannot add new dependents after leaving active service.

Children face an additional restriction. They can only start using transferred benefits after you’ve completed at least 10 years of service, and they must finish the benefit before age 26. A spouse has no age restriction and can use transferred benefits immediately after transfer approval.

| Dependent | Can Use Benefits | Age Limit |

|---|---|---|

| Spouse | Immediately after transfer approval | None |

| Child | After sponsor completes 10 years of service | Must finish by age 26 |

If you’re approaching the 10-year mark and haven’t transferred yet, act now. The four-year additional obligation becomes a serious career calculation at mid-career. Soldiers who transfer at six years and serve to ten get the most flexibility: the obligation is complete and dependents can start using the benefit.

Common Mistakes Soldiers Make

Most GI Bill problems are preventable. The same errors come up repeatedly.

Choosing a school before running the numbers. The GI Bill’s value varies by $20,000 or more depending on school type and location. Look up the MHA for the school’s zip code and calculate the tuition gap before you decide.

Not verifying Yellow Ribbon availability. A school can participate one year and suspend participation the next. Confirm current-year status with the VA’s school finder and the school’s veterans services office directly.

Going fully online without accounting for the MHA cut. Dropping to all-online courses cuts your housing stipend from a local rate to $1,169 flat. If local BAH at your school is $2,400, you leave $1,231 per month on the table every enrolled semester.

Missing the transferability window. The transfer must happen before separation. There’s no retroactive option.

Burning months on light semesters. The GI Bill measures benefit in months, not credit hours. A semester with six credits uses the same benefit as a semester with 18. Load up when your schedule allows.

Not accounting for the housing payment lag. The MHA arrives in arrears. You need at least one month of cash on hand to cover your first month of rent before that payment arrives.

Using the GI Bill with Tuition Assistance

Army Tuition Assistance covers up to $4,500 per year in tuition at $250 per semester credit hour for active-duty soldiers. TA and the GI Bill cannot stack on the same course. TA pays first, and the GI Bill covers whatever TA doesn’t.

The smarter play: use TA to earn credits during service, then preserve GI Bill months for post-service full-time enrollment when the MHA actually pays out. Each GI Bill month you protect while on active duty is a month of housing stipend you’ll collect as a civilian student.

Community college courses and online programs are the easiest way to bank credits on TA. Many soldiers finish associate degrees or 60-plus credit hours before they separate, entering post-service school as a junior or finishing a degree with far fewer GI Bill months burned.

The Complete Guide to Army Pay and Benefits puts the GI Bill in context alongside BAH, BAS, and retirement. The Army benefits guide has current reference figures for TA limits, BAH rates, and GI Bill interaction rules. You may also find Army BAH Rates: How Housing Allowance Works and Army Retirement: BRS Pension Calculator helpful.

This site is not affiliated with the U.S. Army or any government agency. Verify all information with official Army sources before making enlistment or career decisions.