Army Benefits

Army pay is more than a monthly paycheck. Between housing allowances, zero-cost healthcare, education funding, and a pension, active-duty total compensation typically runs $20,000 to $30,000 higher than base pay alone. Add tax-free allowances and free family healthcare and the gap between Army compensation and an equivalent civilian salary grows wider still. This guide covers every major benefit, who qualifies, and how the pieces fit together.

At a Glance

| Benefit | What You Get | Who Qualifies | Learn More |

|---|---|---|---|

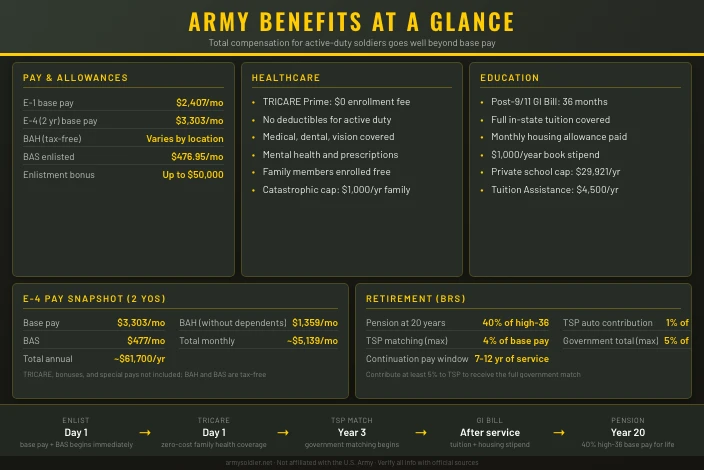

| Base Pay | $2,407/mo (E-1) to $15,408/mo cap, set by grade and years of service | All active-duty soldiers | Army Pay Guide |

| BAH | Tax-free monthly allowance covering local housing costs, based on duty station, pay grade, and dependency status | Soldiers not in government quarters | Army Pay Guide |

| BAS | $476.95/mo (enlisted) or $328.48/mo (officers) in 2026, flat national rate | All active-duty soldiers | Army Pay Guide |

| TRICARE | Full medical, dental, vision, mental health, and prescriptions with zero premiums and zero deductibles for active duty | Active-duty soldiers and enrolled family members | TRICARE Guide |

| Post-9/11 GI Bill | Full in-state tuition, monthly housing allowance, and up to $1,000/year for books | Soldiers with qualifying active-duty service | GI Bill Guide |

| Retirement (BRS) | 40% of high-36 average base pay after 20 years, plus TSP matching up to 5% of base pay | All soldiers under the Blended Retirement System | Retirement Guide |

| Enlistment Bonus | Up to $50,000 for a 6-year contract in a qualifying MOS | Non-prior-service enlistees in SRIP-eligible jobs | Enlistment Bonus Guide |

Which Benefit Matters Most

The right answer depends on your goals and what you plan to do after service.

Education is the priority. The Post-9/11 GI Bill is the most financially valuable long-term benefit for most soldiers. Full in-state tuition at a public university costs nothing out of pocket. The GI Bill also pays a monthly housing allowance based on E-5 BAH rates at the school’s ZIP code, plus $1,000 per academic year for books.

Across four years at a public university, the combined value often exceeds $80,000 depending on location.

Supporting a family now. TRICARE is the most immediately valuable benefit if you have dependents. Active-duty soldiers and their family members pay nothing in premiums, face no annual deductibles, and owe no copays for in-network care. A comparable private-sector family health plan typically costs $500 to $900 per month in premiums alone, not counting copays and deductibles.

Long-term wealth building. The Blended Retirement System works best when you contribute to TSP from day one. The government contributes 1% of base pay automatically and matches your contributions dollar-for-dollar on the first 3% you put in, then 50 cents per dollar on the next 2%. Contribute 5% and you get the full government match.

Pair that with a 20-year pension paying 40% of your average top-36-month base pay for life and you have a wealth-building foundation that most civilian employers do not offer at the same career stage.

Early career, no dependents. If you are young, single, and enlisting for the first time, the enlistment bonus is often the most immediate financial win. High-demand MOS in signal, intelligence, special operations, and maintenance can qualify for $25,000 to $50,000 depending on contract length. That money arrives in installments over the first four years of service.

How Benefits Stack Together

Consider a Specialist (E-4) at two years of service stationed at Fort Sam Houston, Texas. Base pay in 2026 is $3,303 per month. BAH at Fort Sam runs $1,728 with dependents and $1,359 without. BAS adds another $476.95 per month. Neither BAH nor BAS is subject to federal income tax.

Total monthly compensation comes to roughly $5,508 with dependents or $5,139 without. Annualized, that works out to about $66,100 with dependents or $61,700 without, while also receiving full family healthcare for free.

Soldiers serving in a combat zone get a further tax advantage. Under the Combat Zone Tax Exclusion, enlisted soldiers pay no federal income tax on base pay for every month they serve in a designated combat zone. For an E-4 earning $3,303 a month, a 9-month deployment can save over $7,000 in federal taxes at a standard marginal rate.

Over a career, these advantages compound. Annual pay raises adjust base pay every January 1. BAH increases when you move to higher-cost duty stations or get promoted. Special pays for hazardous duty, flight operations, or foreign language skills stack on top.

When Benefits Start

Not all Army benefits are available immediately, and some build value over time. Knowing which benefits are immediate and which require service milestones helps with financial planning before you enlist.

Benefits available from your first day of active duty:

- Base pay starts the day you enter active duty

- BAH applies when you are assigned to a duty station without government quarters

- BAS is paid monthly from your first day of active service

- TRICARE Active Duty coverage begins the moment your active duty starts : your enrolled family members are covered from the same date

- Servicemembers Civil Relief Act (SCRA) protections : including a 6% interest rate cap on pre-service debts and certain eviction protections : apply immediately upon active duty entry

Benefits that require time or qualifying service:

- Post-9/11 GI Bill requires at least 90 days of service after September 10, 2001. To qualify at 100% : covering full in-state tuition at a public school : you need 36 or more months of qualifying service.

- Enlistment bonus installments follow a schedule: 50% after completing your training pipeline, 25% at your second service anniversary, and 25% at your fourth.

- TSP government matching begins after 60 days of service. The automatic 1% government contribution starts on day one, but the matching contributions require you to contribute your own money first.

- Retirement pension under the Blended Retirement System requires 20 qualifying years. The BRS pension does not prorate for shorter service : soldiers who leave before 20 years keep their TSP balance but receive no pension.

Understanding this timeline prevents surprises. A soldier who completes a standard 4-year enlistment and separates will leave with their GI Bill benefit, TSP balance, and any remaining bonus installments : but no pension.

Reserve and National Guard Benefits

Reserve and Guard soldiers receive a different and more limited benefit package, tied primarily to drilling status and federal activation status.

Drilling reservists receive:

- Drill pay for one weekend per month and two weeks of annual training, calculated on the same pay-grade schedule as active duty

- TRICARE Reserve Select at a premium cost (not free as on active duty) : $57.88 per month for the soldier only in 2026, more with dependents

- GI Bill Chapter 1606 upon completing a 6-year Reserve or Guard obligation : pays $493 per month at full-time enrollment, about one-fifth of what Ch. 33 pays

When federally activated:

- Full active-duty pay, BAH, and BAS apply for the duration

- TRICARE Active Duty replaces TRICARE Reserve Select at no premium cost

- SCRA protections apply during activations

State activations (Guard soldiers called up by the governor) do not trigger full federal benefits. Pay comes from the state and federal TRICARE does not apply.

Reserve and Guard soldiers who accumulate 20 qualifying years of service earn a retirement pension, available at age 60. The amount is calculated differently from the active-duty formula and reflects part-time rather than continuous service. For a detailed comparison of how full-time and part-time service affect benefits, see active duty vs. Army Reserve vs. National Guard.

How Army Pay Compares to Civilian Salaries

A direct comparison between Army base pay and a civilian salary is misleading because it ignores tax treatment, benefits costs, and deferred compensation.

Tax advantage on allowances. BAH and BAS are not subject to federal income tax. An E-4 receiving $1,728 in BAH keeps the full amount; a civilian employee receiving the same as part of compensation pays income tax on it. On $22,032 in annual allowances at a 22% combined rate, that difference is roughly $4,800 per year in additional effective compensation.

Healthcare cost replacement. A comparable civilian family health plan costs $8,000 to $15,000 per year in employee premiums and out-of-pocket costs. Active-duty TRICARE charges nothing in premiums and no deductibles for in-network care. That benefit alone converts what appears to be a below-market salary into one that effectively pays $8,000 to $15,000 more per year than the base pay number implies.

Deferred compensation. Under the Blended Retirement System, the government contributes up to 5% of base pay annually to the soldier’s TSP account. On an E-5 base pay of $3,599, that is up to $2,159 per year in government contributions that compound regardless of whether the soldier reaches 20 years. A 20-year career produces a lifetime pension beginning at separation : a form of deferred compensation most civilian employers do not offer to workers at the 20-year mark in comparable roles.

Soldiers who account for these components when evaluating a civilian job offer often find the gap is smaller than the salary numbers suggest, particularly when TRICARE replaces a high-cost employer health plan and BAH covers housing in full.

Benefits Directory

These guides cover each benefit in detail. Start with the one that matches your current priority. Reading the pay guide and retirement guide together gives the clearest picture of total compensation over a full career; reading the GI Bill and TRICARE guides together clarifies post-service transition costs and the timing decisions that affect how much of each benefit you actually receive.

- Army Pay Guide: Base pay tables, BAH, BAS, and special pays for active-duty soldiers in 2026

- Enlistment Bonus Guide: How much you can earn, which MOS qualify, and how bonuses are structured and paid

- TRICARE Guide: Zero-cost health coverage for active-duty soldiers and their families

- GI Bill Guide: Tuition, housing allowance, and book stipend under the Post-9/11 GI Bill

- Retirement Guide: BRS pension, TSP matching, and long-term savings planning

For a deeper look at how the pieces fit together in dollar terms, how Army pay and benefits add up for a real soldier walks through total compensation scenarios for different life situations.

Explore more Army guides covering paths to serve and test prep resources.