Army Retirement and the Blended Retirement System

Army retirement has two systems. If you entered service before January 1, 2018, you’re on the Legacy High-36 system unless you opted into BRS. If you entered on or after that date, you’re under the Blended Retirement System (BRS). Understanding which one applies to you and how it works affects every financial decision you make during your career.

The Two Systems

Legacy (High-36): A pure pension system. Serve 20 years, receive a monthly pension for life. Leave before 20 years, receive nothing from the military retirement system. No government TSP contributions.

Blended Retirement System (BRS): A hybrid. A slightly lower pension rate, plus automatic government TSP contributions and matching during your career. You receive something even if you leave before 20 years, as long as you served long enough to vest.

Nearly all soldiers entering service today are under BRS. The opt-in window for prior-service members closed December 31, 2018.

BRS Pension

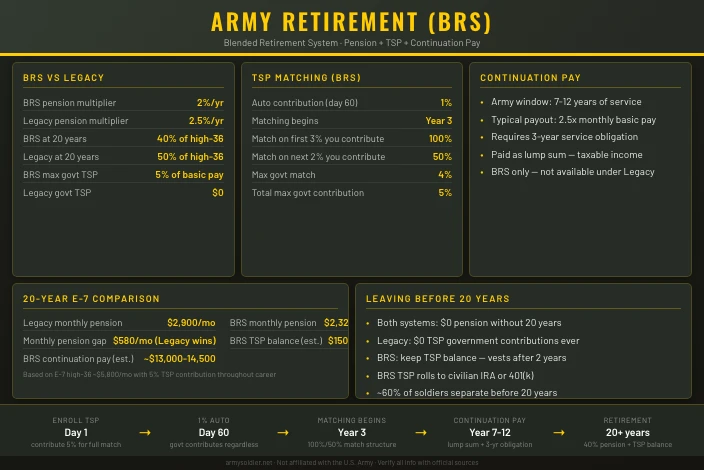

The BRS pension formula is 2% per year of service, multiplied by your average basic pay over the highest 36 months of your career (the high-36 average).

At exactly 20 years: 2% x 20 = 40% of your high-36 average basic pay.

An E-7 retiring at 20 years with a high-36 average of approximately $5,800 per month would receive:

- Monthly pension: 40% x $5,800 = $2,320/month

Each additional year beyond 20 adds another 2%. Serve 22 years and you receive 44% of high-36 instead of 40%. Serve 30 years and you receive 60%.

At retirement you can elect a lump sum option: receive 25% or 50% of the actuarial present value of your pension as a one-time payment. Your monthly annuity is then reduced until age 67, when it returns to the full calculated amount. Most retirees skip this option because the reduction in monthly pay is steep relative to the lump sum received.

Legacy Pension

The Legacy pension formula is 2.5% per year of service. At 20 years, that’s 50% of high-36.

Using the same E-7 example with a high-36 of $5,800:

- Monthly pension: 50% x $5,800 = $2,900/month

That’s $580 per month more than BRS, paid for life. The tradeoff is that Legacy soldiers receive zero government TSP contributions during their career.

At 30 years, the Legacy formula reaches 75% of high-36. BRS reaches 60% at 30 years.

TSP Matching Under BRS

The TSP (Thrift Savings Plan) is the government’s 401(k) equivalent. Under BRS, the government makes automatic and matching contributions to your account.

Automatic 1% contribution. Starting 60 days after you enter service, the government deposits 1% of your basic pay into your TSP every month, whether or not you contribute anything yourself. This contribution vests after 2 years of service.

Matching contributions. Starting at the beginning of your 3rd year of service, the government matches your contributions at these rates:

| Your Contribution | Government Match |

|---|---|

| 1% | 1% |

| 2% | 2% |

| 3% | 3% |

| 4% | 3.5% |

| 5% | 4% |

The maximum government match is 4% of basic pay, reached when you contribute 5%. Combined with the 1% automatic contribution, the total government contribution tops out at 5% of basic pay.

To get the full match, you must contribute at least 5% of your basic pay. Contributing less means leaving government money behind.

An E-4 earning $3,303/month and contributing 5% ($165/month) gets an additional $165/month from the government, for $330/month total going into TSP. Over 10 years at that contribution level, that’s roughly $39,600 in combined contributions before any investment growth.

Continuation Pay

Continuation Pay is a one-time lump sum payment available only under BRS, offered to soldiers at the mid-career point. It’s designed to keep soldiers past the 10-year mark when many consider leaving service.

| Factor | Details |

|---|---|

| Army active component window | 7 to 12 years of service |

| Typical multiplier | 2.5x monthly basic pay |

| Multiplier range | 2.5x to 13x (Army sets annually by MOS) |

| Service obligation | 3 additional years minimum |

| Tax status | Taxable income |

An E-7 at 10 years earning $5,268/month would receive approximately $13,170 at the typical 2.5x multiplier, in exchange for a 3-year service obligation.

Continuation pay is taxable income. You can deposit it directly into TSP up to the annual IRS contribution limit, which reduces the immediate tax impact and puts the money to work inside a tax-advantaged account.

BRS vs. Legacy: Direct Comparison

Two scenarios: a soldier who serves exactly 20 years, and one who leaves at 10 years.

E-7 retiring at 20 years (high-36 ~$5,800/month):

| Factor | Legacy | BRS |

|---|---|---|

| Pension multiplier | 2.5%/yr | 2.0%/yr |

| Monthly pension | $2,900 | $2,320 |

| Pension difference | – | -$580/mo |

| Govt TSP during career | $0 | 1% auto + up to 4% match |

| Estimated TSP balance | $0 | $150,000+ |

| Continuation pay | $0 | ~$13,000-14,500 |

The Legacy soldier has a higher pension for life. The BRS soldier has a lower pension but a TSP balance to draw from. At $580/month lower pension, the BRS soldier would need the TSP balance to last approximately 22 years to break even on total dollar value. A well-invested TSP can generate income that partially offsets the pension difference.

Soldier who leaves at 10 years:

| Factor | Legacy | BRS |

|---|---|---|

| Pension | $0 | $0 |

| Govt TSP contributions | $0 | 1% auto + matching (years 3-10) |

| Estimated TSP balance | $0 | $40,000-60,000+ |

| Portable to civilian IRA/401(k) | N/A | Yes |

The 10-year Legacy soldier leaves with nothing from the military retirement system. The 10-year BRS soldier leaves with a TSP balance they own outright and can roll into a civilian IRA or 401(k). This is where BRS has a clear advantage: it gives every soldier something for their service, not just those who reach 20 years.

The roughly 60% of soldiers who separate before 20 years get zero benefit from Legacy retirement. BRS was designed specifically to address that problem.

Pension Vesting and the 20-Year Requirement

Both systems require 20 years of service to receive any pension. BRS did not eliminate the 20-year cliff for the pension component. What BRS changed is that the TSP portion is portable and has value even without a pension.

Year 2: The 1% automatic TSP contribution vests. If you separate after 2 years, you keep that balance.

Year 3: Government TSP matching begins. From this point forward, contributing 5% gets you the full 4% government match on top of the 1% auto.

Year 19 under Legacy: Leaving one year short means $0 pension and $0 TSP government contributions ever received.

Year 19 under BRS: Still no pension, but you keep all vested TSP contributions accumulated from years 2 through 19. That balance rolls into a civilian IRA or 401(k) when you separate.

What to Do Under BRS

Contribute at least 5% to TSP from day one. The government match doesn’t begin until year 3, but the 1% auto contribution starts at 60 days. Starting contributions early maximizes growth time before matching kicks in.

Increase contributions at every promotion. Every pay raise is an opportunity to put more into TSP before lifestyle spending absorbs the difference. Even a 1% increase at E-5 adds up over a full career.

Invest continuation pay into TSP. When you receive it at the 7-12 year window, deposit a portion directly into TSP up to the annual IRS limit. The lump sum invested now grows for potentially another decade before you retire.

Run the break-even numbers before year 10. The BRS calculator at militaryonesource.mil lets you compare projected outcomes at different separation points. Run it when you’re deciding whether to accept continuation pay or re-enlist.

Survivor Benefit Plan

The Survivor Benefit Plan (SBP) is a separate decision you make at retirement, not during your career. It reduces your monthly pension by up to 6.5% in exchange for covering a portion of that pension to your surviving spouse after your death.

Without SBP, your military pension stops the day you die. Your spouse receives nothing from it. With SBP at full coverage, your spouse receives 55% of your retired pay for the rest of their life. The premium is paid from your pension before you see it.

SBP is a significant financial decision that depends on your spouse’s other income sources, life insurance, age gap, and health. Most retirees with spouses elect at least partial SBP coverage. Review the detailed terms at dfas.mil/survivor before your retirement ceremony, not after.

Reserve and National Guard Retirement

Reserve and National Guard soldiers follow a different retirement structure. Instead of 20 years of active duty, they earn retirement points for each year of service. A qualifying year requires a minimum number of retirement points earned through drills, annual training, and active duty periods.

Reserve and Guard members don’t draw their pension immediately at the 20-qualifying-year mark. They receive a gray area retirement, where they are retired but must wait until age 60 to begin collecting monthly pay. Under BRS, TSP contributions and matching follow the same rules during any period of active duty orders, and the TSP balance is available at standard retirement ages.

The exact point calculation and early draw eligibility for Reserve retirement are at va.gov and hrc.army.mil.

This site is not affiliated with the U.S. Army or any government agency. Verify all information with official sources at militaryonesource.mil, dfas.mil, and tsp.gov before making retirement or financial decisions.

For more on Army benefits, see the benefits overview, Post-9/11 GI Bill education benefits, and TRICARE health coverage.