Post-9/11 GI Bill Guide

The Post-9/11 GI Bill is the most valuable education benefit the Army offers. If you served 90 days of active duty after September 10, 2001, you’ve likely earned it. This guide covers exactly what it pays for, what it doesn’t, and how it compares to the two other GI Bill programs you may encounter.

What It Covers

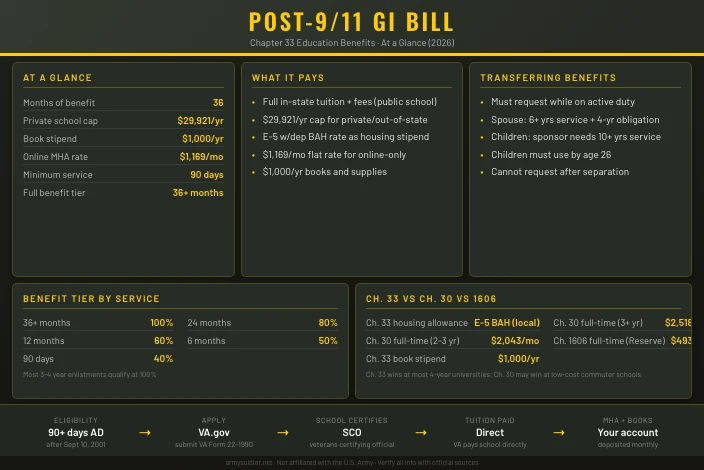

The benefit has three separate parts: tuition coverage, a monthly housing allowance, and a book stipend. Each is paid independently.

Tuition and fees. At a public school, VA pays your full in-state tuition and mandatory fees with no dollar cap. At private schools or out-of-state public schools, the cap is $29,920.95 for academic year 2025-2026. VA has not yet published the AY 2026-2027 cap as of March 2026; that rate typically releases in August each year.

Monthly Housing Allowance (MHA). While enrolled more than half-time, VA pays a monthly housing allowance equal to the E-5 with dependents BAH rate for the ZIP code where your school is located. The amount varies by location. A school in a high-cost city pays considerably more than a school in a rural area. For online-only enrollment, the rate is a flat $1,169 per month regardless of location. The housing allowance is paid directly to you, not to the school.

To make this concrete: a veteran attending a state university in a city where the E-5 with dependents BAH is $1,800 per month receives that $1,800 every month while enrolled full-time. At a school in a higher-cost area where E-5 BAH is $2,400, they’d receive $2,400. This BAH stipend alone often covers rent and most living expenses.

Books and supplies. VA pays up to $1,000 per academic year for books and supplies. The payment is prorated to your enrollment level.

You get 36 months of benefits total. That’s enough for a standard 4-year degree if you attend full-time.

Eligibility and Benefit Tiers

You need at least 90 days of active duty service after September 10, 2001, followed by an honorable discharge. If you separated due to a service-connected disability, that counts regardless of time served.

Your benefit level scales with how long you served:

| Service After 9/10/2001 | Benefit Level |

|---|---|

| 36 or more months | 100% |

| 30 months | 90% |

| 24 months | 80% |

| 18 months | 70% |

| 12 months | 60% |

| 6 months | 50% |

| 90 days to 6 months | 40% |

At 100%, you get full in-state tuition at public schools and the full private school cap. At lower tiers, all three benefits scale proportionally. Most soldiers who complete a standard 3- or 4-year enlistment qualify at 100%.

Yellow Ribbon Program

The Yellow Ribbon Program covers tuition above the private school cap. A participating school contributes money toward your excess tuition cost, and VA matches that contribution dollar-for-dollar. There’s no cap on the VA match, so the combined school contribution and VA match can cover any amount above $29,920.95.

To use Yellow Ribbon, both conditions must be met:

- You must be eligible at the 100% benefit tier

- Your school must participate and have an available slot for the current academic year

You qualify at the 100% tier through one of these paths:

- 36 or more months of active duty service after September 10, 2001

- Honorable discharge due to a service-connected disability

- Purple Heart award

Not every private school participates, and those that do limit their Yellow Ribbon slots each year. If a school’s page says “unlimited” slots, you’re in good shape. Schools that cap slots at 10 or 20 per year can fill quickly. Confirm availability with the school’s veterans services office before committing to enrollment.

Kicker and MGIB Buy-Up

Army College Fund (kicker). Some enlistment contracts include an Army College Fund, commonly called a kicker. The kicker adds a fixed monthly amount on top of the standard MGIB-AD payment. The amount is negotiated at enlistment and varies by MOS and recruiting need. Kickers can range from a few hundred to over a thousand dollars per month added to the base MGIB rate.

MGIB Buy-Up. This option lets you pay an additional $600 during service (in increments of $20 to $100) to increase your monthly MGIB-AD rate by up to $150 per month. The $150/month increase over 36 months returns $5,400, making the Buy-Up worthwhile if you plan to use MGIB-AD rather than switch to Ch. 33.

Neither the kicker nor the Buy-Up carry over if you switch to Ch. 33. If you paid into MGIB-AD and then elect Ch. 33, you lose access to those added benefits and you don’t recover the $1,200 MGIB contribution. For most students, Ch. 33’s housing allowance more than compensates for the loss, but it’s worth doing the math for your specific school and location.

Transferring to Dependents

Active duty service members can transfer unused Ch. 33 benefits to a spouse or dependent children before separating. Rules differ by family member.

Spouses can receive transferred benefits once the sponsor has 6 or more years of service. The sponsor must also commit to 4 additional years of service at the time of transfer. Spouses can begin using the benefit immediately after the transfer is approved.

Children can receive transferred benefits only after the sponsor completes 10 years of service. They can’t use those benefits before that threshold is reached, and they must use them by age 26.

You must request the transfer through milConnect while still on active duty or in the Selected Reserve. There is no way to request the transfer after you separate.

Ch. 33 vs. Ch. 30 vs. Ch. 1606

Three GI Bill programs exist. You can only use one at a time, and switching has trade-offs.

| Feature | Ch. 33 (Post-9/11) | Ch. 30 (MGIB-AD) | Ch. 1606 (Selected Reserve) |

|---|---|---|---|

| Who qualifies | Active duty 90+ days post-9/10/2001 | Active duty; paid $1,200 during service | 6-year Reserve or Guard obligation |

| Tuition benefit | Full in-state or $29,920.95/yr cap (private) | None | None |

| Full-time monthly rate | N/A (pays school directly) | $2,518/mo (3+ yr) / $2,043/mo (2-3 yr) | $493/mo |

| Housing allowance | E-5 w/dependents BAH at school ZIP | None | None |

| Book stipend | $1,000/year | None | None |

| Months of benefit | 36 | 36 | 36 |

| Transferable to dependents | Yes (with service obligation) | No | No |

Ch. 33 wins at most 4-year universities because the housing allowance plus tuition coverage exceeds the flat Ch. 30 rate. Ch. 30 can come out ahead at low-cost commuter schools, especially in low-BAH areas, where the $2,518 monthly stipend exceeds what Ch. 33’s housing allowance would total.

Ch. 1606 is the option for Guard and Reserve members who haven’t served enough active duty to qualify for Ch. 33. At $493 per month for full-time enrollment, it covers a portion of tuition costs and pays about one-fifth of what Ch. 30 MGIB-AD pays. It’s designed for part-time students balancing civilian jobs and drill schedules, not as a replacement for active duty GI Bill programs.

Applying

Gather these before you start:

- DD-214 (if separated) or a statement of active duty service (if currently serving)

- Your school’s VA facility code (on the school’s veterans services page)

- Banking information for direct deposit

Then follow these steps:

- Submit VA Form 22-1990 at va.gov/education/apply-for-education-benefits.

- Confirm your school is VA-approved using the VA’s WEAM Institution Search at inquiry.vba.va.gov.

- Contact your school’s veterans certifying official (SCO) and tell them you’re using Ch. 33. They’ll certify your enrollment to VA.

- VA processes the claim. Processing typically takes 4 to 8 weeks from the date VA receives the certification.

- Once approved, tuition payments go directly to the school. MHA and book stipend payments deposit into your bank account.

Keep your enrollment status current with both your SCO and VA. Changes in credit hours mid-semester affect your MHA payment. An overpayment from VA creates a debt you’ll have to repay, so report schedule changes promptly.

This site is not affiliated with the U.S. Army or any government agency. Verify all information with official Army and VA sources before making enrollment or benefits decisions.

For more on Army benefits, see the benefits overview, TRICARE health coverage, and Army retirement and the Blended Retirement System.