TRICARE Health Coverage Guide

TRICARE is the military’s health care program. If you’re on active duty, the coverage costs nothing. If you’re in the Reserve or Guard, you pay a monthly premium, but far less than a typical civilian employer plan. Understanding which plan applies to your situation, what it costs, and what it covers prevents costly surprises when you need care.

Who Gets TRICARE

TRICARE covers five categories of beneficiaries. The cost level depends on which category you fall into:

| Beneficiary Category | Eligibility | Cost Level |

|---|---|---|

| Active duty service member | All ranks, all components | Free (TRICARE Prime) |

| Active duty family member | Registered in DEERS | Free or low cost |

| Reserve/Guard member | Not on orders over 30 days | Premium-based (voluntary) |

| Retiree | 20+ years active duty | Annual enrollment fee |

| Retiree family member | Registered in DEERS | Annual enrollment fee |

Active duty service members are automatically enrolled in TRICARE Prime at no cost. Family members must be registered in the Defense Enrollment Eligibility Reporting System (DEERS) to receive coverage. Registration happens at your installation ID card office or online through milConnect.

Coverage changes when you separate. Active duty status ends TRICARE Prime eligibility. The Enrolling and Making Changes section below covers what to do and when.

TRICARE Prime

TRICARE Prime is the managed care option. It works like an HMO: you’re assigned a primary care manager at either a military treatment facility (MTF) or a civilian network provider, and most care is coordinated through them.

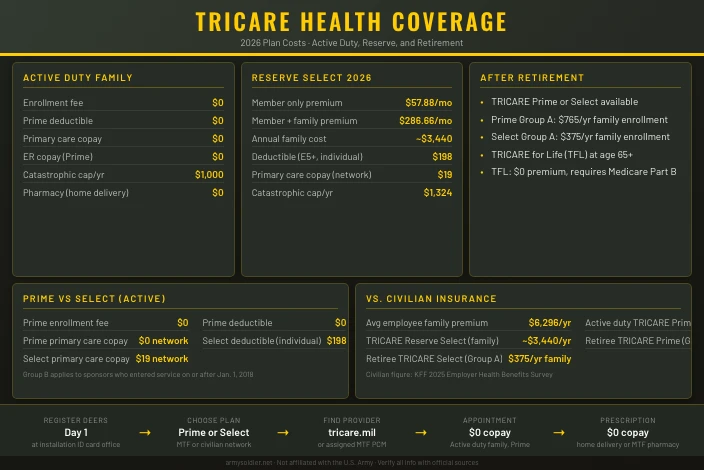

For active duty service members, Prime has zero cost at every level. No enrollment fee, no deductible, no copay for network care.

For active duty family members, Prime also has no enrollment fee. The deductible and copay structure depends on when your sponsor entered service:

Group B (sponsor entered service on or after January 1, 2018):

| Cost Item | Amount |

|---|---|

| Enrollment fee | $0 |

| Deductible | $0 |

| Primary care copay (network) | $0 |

| Emergency room copay (network) | $0 |

| Catastrophic cap (family/year) | $1,000 |

Group A (sponsor entered service before January 1, 2018):

Enrollment fee is $0, deductible is $0, and primary care copay for network visits is $0. The annual catastrophic cap differs and is listed in the TRICARE Costs and Fees sheet at tricare.mil.

For retirees and their families, Prime is still available but requires an enrollment fee:

| Retiree Plan | Individual/Year | Family/Year |

|---|---|---|

| Prime (Group A) | $381.96 | $765.00 |

| Prime (Group B) | $462.96 | $927.00 |

Retirees on Prime pay $26 per primary care visit in network (Group A) with no annual deductible. The catastrophic cap and specialist copays are on the TRICARE cost sheet at tricare.mil.

TRICARE Select

TRICARE Select is the preferred provider option. It gives you more freedom to see providers without a referral, but you pay more when you use it. There’s no primary care manager assignment under Select.

For active duty family members, Select has no enrollment fee but applies deductibles and copays:

| Select (Active Duty Family, Group B) | E1-E4 | E5+ |

|---|---|---|

| Annual deductible (individual) | $66 | $198 |

| Annual deductible (family) | $132 | $397 |

| Primary care copay (network) | $19 | $19 |

| Emergency room copay (network) | $52 | $52 |

| Catastrophic cap (family/year) | $1,324 | $1,324 |

For retirees:

| Retiree Select | Individual/Year | Family/Year |

|---|---|---|

| Select (Group A) | $186.96 | $375.00 |

| Select (Group B) | $594.96 | $1,191.00 |

Group A retirees on Select pay a $150 individual / $300 family annual deductible and $38 per primary care visit in network.

The choice between Prime and Select usually comes down to access. Prime costs less out of pocket but requires referrals for specialists. Select lets you go directly to a network specialist, which matters if you have ongoing specialty care needs.

TRICARE Reserve Select

Reserve and Guard members who aren’t on active duty orders of more than 30 days can purchase TRICARE Reserve Select. It’s a voluntary premium-based plan with coverage comparable to Select.

2026 TRICARE Reserve Select premiums:

| Coverage | Monthly | Annual |

|---|---|---|

| Member only | $57.88 | $694.56 |

| Member plus family | $286.66 | $3,439.92 |

Deductibles and copays under Reserve Select match the Group B Select structure:

| Reserve Select | E1-E4 | E5+ |

|---|---|---|

| Annual deductible (individual) | $66 | $198 |

| Annual deductible (family) | $132 | $397 |

| Primary care copay (network) | $19 | |

| Catastrophic cap (family/year) | $1,324 |

When you activate for orders longer than 30 days, you become eligible for active duty TRICARE Prime at no cost. You can suspend Reserve Select during that period and reinstate it when you return to inactive status. Contact your TRICARE regional contractor to manage the transition.

Reserve Select is worth comparing to civilian employer plans. A reservist with a family paying $286.66 per month ($3,440 per year) for Reserve Select gets coverage with deductibles and copays in line with a mid-tier civilian PPO. Civilian family premiums for comparable coverage often run $500 to $700 per month in employee contributions alone. If your civilian employer offers health coverage, run the numbers both ways before enrolling. Some employer plans are better; many are not.

TRICARE for Life

TRICARE for Life (TFL) is the coverage for military retirees who are 65 or older and enrolled in both Medicare Part A and Part B. It works as a Medicare supplement: Medicare pays first, and TFL covers most of the remaining cost-sharing.

| Cost Item | Amount |

|---|---|

| TFL enrollment fee | $0 |

| Medicare Part B monthly premium | ~$185/month (2026 standard) |

| TFL individual deductible | $150 |

| TFL family deductible | $300 |

TFL covers much of what Medicare doesn’t: Part A and Part B cost-sharing, hospice coinsurance, and some foreign travel emergency coverage. Most TFL beneficiaries pay very little out of pocket because TFL absorbs the gaps Medicare leaves behind.

You don’t need to separately enroll in TFL. It activates automatically once you’re in DEERS and enrolled in Medicare Part B. The critical step is enrolling in Medicare Part B on time. If you miss the initial enrollment window (the 7-month period around your 65th birthday), you’ll face late enrollment penalties and a coverage gap. Enroll in Medicare Part B before you turn 65 if you want uninterrupted TFL coverage the day you’re eligible.

Dental Coverage

Dental coverage works differently for each beneficiary group:

| Who | Dental Option | Cost |

|---|---|---|

| Active duty member | Military dental facility | Free |

| Active duty family member | TRICARE Dental Program (TDP) | Monthly premium + cost-share |

| Reserve/Guard member | TRICARE Dental Program (TDP) | Monthly premium + cost-share |

| Retiree and family | FEDVIP (voluntary) | Separate enrollment fee |

The TRICARE Dental Program (TDP) is a voluntary plan for active duty families and Guard and Reserve members. It covers preventive care (cleanings, X-rays), basic restorative care (fillings), and major restorative care (crowns, extractions) with cost-sharing percentages that vary by service type. TDP is not free, but the premiums are subsidized for active duty families. Current premiums and the cost-sharing schedule are at tricare.mil/dental.

Retirees and their families are not eligible for TDP. The Federal Employees Dental and Vision Insurance Program (FEDVIP) is available to retirees as a separate voluntary dental option, with premiums varying by plan and coverage level.

Vision Coverage

TRICARE covers vision care in two tiers: medically necessary and routine. What’s covered depends on who you are:

| Service Type | Active Duty Member | Family Member / Retiree |

|---|---|---|

| Medically necessary (eye disease, injury) | Covered | Covered |

| Routine eye exam (glasses, contacts) | Covered | Not covered as standard benefit |

| Eyeglasses/contacts | Covered | Not covered |

Medically necessary vision care, such as treatment for glaucoma, retinal conditions, or eye injuries, is covered under all TRICARE plans for all beneficiaries. Routine exams for a new prescription fall outside that definition for family members and retirees.

Family members and retirees who want routine vision coverage typically add FEDVIP or a private vision plan. FEDVIP offers several vision plan options at fedvip.com and is available to retirees, reservists on qualifying orders, and some other categories.

How TRICARE Compares to Civilian Insurance

The cost difference between TRICARE and civilian employer coverage is significant, especially for families.

The average employee share for family coverage on a civilian plan ran $6,296 per year in 2025. The full premium, employer and employee combined, averaged roughly $24,000 per year.

| Coverage | Annual Cost (family) |

|---|---|

| Active duty TRICARE Prime | $0 |

| TRICARE Reserve Select (family) | $3,440 |

| TRICARE Prime, retiree (Group A) | $765 |

| TRICARE Select, retiree (Group A) | $375 |

| Avg. employee share, civilian family plan | $6,296 |

Active duty coverage is a full family health plan at zero cost for network care. Even TRICARE Reserve Select at $3,440 per year costs less than the typical employee share alone on a civilian family plan. For a Reserve soldier considering whether the time commitment is worth the benefits, health coverage at roughly $287 per month for the entire family is one of the more concrete numbers.

Enrolling and Making Changes

Enrollment steps differ by situation:

Active duty (automatic). Service members are enrolled in TRICARE Prime automatically. Register family members in DEERS at your installation ID card office or at milconnect.dmdc.osd.mil. Family enrollment is not automatic and must be done within 60 days of a qualifying life event (marriage, birth, adoption).

PCS moves. Prime enrollment transfers automatically during a Permanent Change of Station move, but your primary care manager assignment changes to the new duty station. Update your PCM at tricare.mil after arriving at the new installation to avoid delays in care.

Separating or retiring. You have 90 days after your separation date to enroll in a retiree TRICARE plan (Prime or Select). After that window closes, you must wait for open enrollment. Some separating members qualify for the Transitional Assistance Management Program (TAMP), which provides 180 days of continued active duty-level TRICARE coverage. Check eligibility at tricare.mil/eligibility.

Reserve members. You can enroll in TRICARE Reserve Select at any time once you meet eligibility requirements. If you activate for more than 30 days, your eligibility shifts to active duty TRICARE Prime and you can suspend Reserve Select for that period.

Your TRICARE region (East or West) determines which contractor handles your claims. Benefits and federal cost standards are the same regardless of region. Find your regional contractor at tricare.mil.

This site is not affiliated with the U.S. Army or any government agency. Verify all information with official sources at tricare.mil and health.mil before making health coverage decisions.

For more on Army benefits, see the benefits overview, Post-9/11 GI Bill education benefits, and Army retirement and the Blended Retirement System.